Robinhood's Latest Quest

Robinhood's Latest Quest

Is the new Gold credit card really a bullseye?

Hi Shreycationers,

This week I was gonna talk about how to hack basic economy, but then Robinhood upended those plans when they dropped one of their biggest announcements in years: a 3% cash back credit card.

I mean she is truly a stunning card. But looks aren’t everything. Let’s dive in and see what this card is made of.

(It’s made of 17 grams of stainless steel.)

(Disclaimer: This post is not financial advice and you should do your own research to ensure the cards mentioned in this article are right for you. Applying will likely affect your credit score.)

What’s great

First things first, Robinhood’s done a great job stealing headlines with this card, and it’s not just all show. This is indeed a wonderfully designed card.

A simple 3% cash back on everything

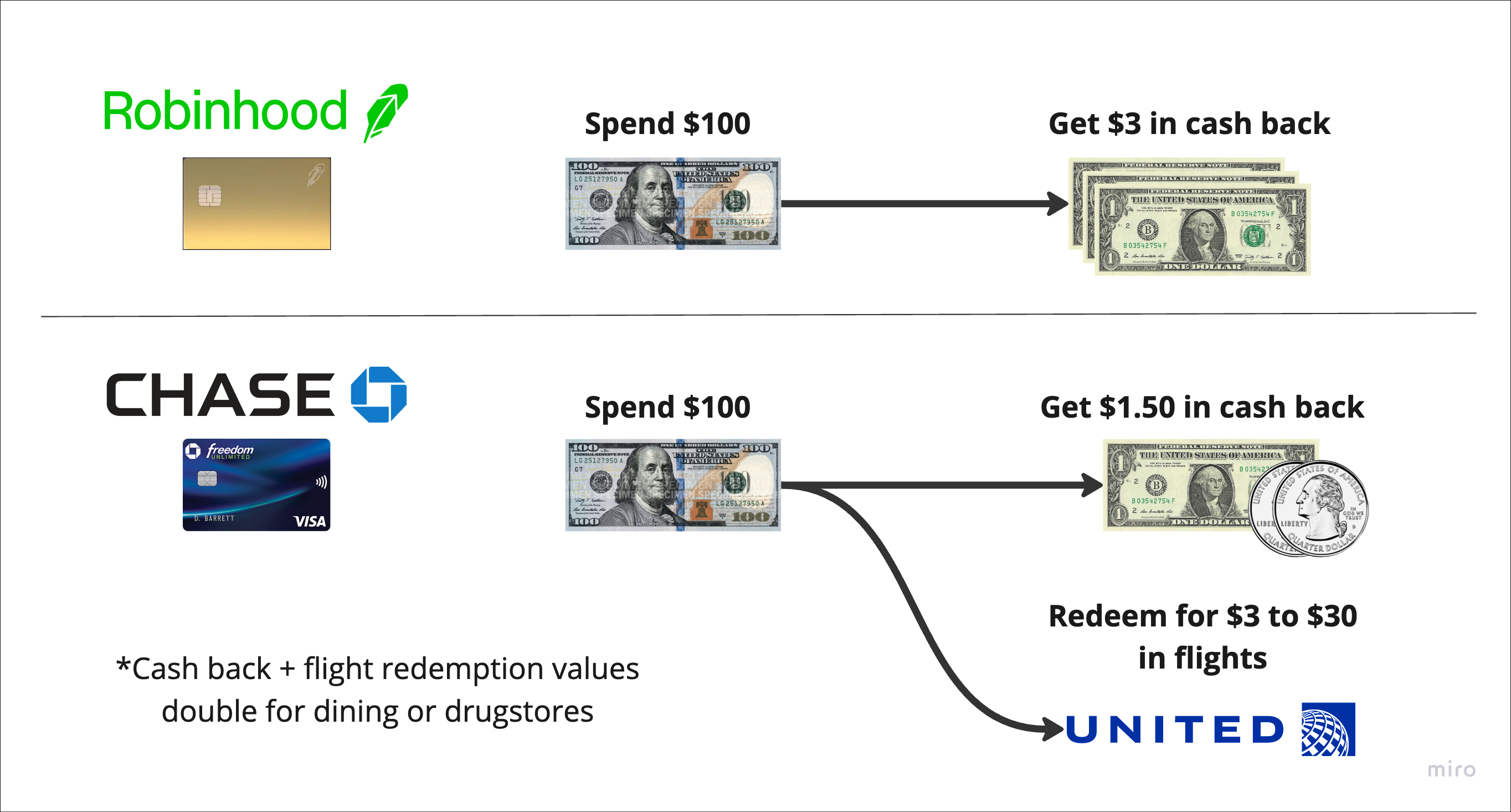

Everyone’s talking about the flagship feature, the 3% cash back on everything. And with good reason: 3% is the highest base cash back rate across any card I’ve seen. There’s not much else to say here — it’s truly a great cash back rate with no hoops to jump through. There’s something refreshing about the simplicity here, and it’s especially great for beginners.

But there’s other features that didn’t get as much attention and are also worth highlighting.

No foreign transaction fees

No foreign transaction fees means you can truly use this card to earn 3% on everything, including that shopping spree in Milan.

Waiving foreign transaction fees used to limited to high annual fee cards, but recently low/no annual fee cards have been introducing it too, including the Apple Card and the Capital One Quicksilver. The Robinhood Gold card is by far the most versatile and valuable of these though. For those who don’t like to carry many cards, you can now ditch whatever low annual fee, no foreign transaction fee card you might have and get 3% on your abroad expenses instead.

Spend using Virtual Cards

This is actually the perk I’m most excited for with this card, because as far as I know, no other card on the market offers native virtual cards.

Virtual cards let you hide your true credit card number when spending online, and allow you to set an expiry date and spending limit. The killer use case here is managing subscriptions: if you just want 1 month of Hulu to binge Shogun, you can load a virtual card with $8 and have it expire in a month. If you forget to cancel your subscription, it won’t matter; your payment method will be invalid by the month’s end anyway.

Virtual card services like Privacy have existed for a while, but as third party services they’re not as convenient, and their free offerings aren’t as robust as what Robinhood seems to be providing here.

Surprising amount of protections

The Robinhood Gold card is part of the Visa Signature family, which comes with various optional benefits that credit card providers can activate. I’m happy to say Robinhood really went for extra credit here; this card is loaded with benefits, including:

Purchase security: If you buy something nice and it gets lost or stolen in 90 days, you can get up to $1k back.

Extended warranties: You can extend the warranty of new purchases by up to a year.

Return protection: If you aren’t satisfied with a recent purchase and the store won’t take it back, you can get reimbursed up to $250.

Trip cancellation protection: If you get injured before or during a trip, you can get up to $2k to cover nonrefundable arrangements.

Auto rental collision damage waiver: You can skip the insurance at the rental car office when you use you card to rent.

Many other low annual fee cards have some subset of these perks, but Robinhood is giving you basically everything. If you’ve got premium cards like an Amex platinum, you likely already have access to many of these perks (and with better limits), but this is still spectacular for what is effectively a starter card. The only notable perk that’s missing here is cell phone protection (get reimbursed if your phone is lost/stolen).

5% cash back when booking travel

…but that travel has to be booked through Robinhood’s forthcoming travel portal. Now if you’ve used these travel portals through Chase or Amex or other cards, you know these portals aren’t that fun or convenient to use. Also, sometimes these portals don’t have the flights and hotels you’re interested in. Robinhood’s portal isn’t live so it’s hard to make judgements quite yet, but something tells me it won’t be groundbreaking here.

5% cash back has been emerging as a popular number for spend in travel portals, so this number isn’t as groundbreaking as the 3% cash back. You’ll earn the same with a Chase Freedom or a Capital One Quicksilver. But still, 5% is 5%, and it’s good to see Robinhood meeting the industry standard here.

What’s not so great

You need Robinhood Gold…and you need to maintain it

The card’s $0 annual fee branding is a little bit misleading. In order to get the card, you’ll need to be a Robinhood Gold subscriber. But you also need to maintain Robinhood Gold to keep the card.

This will be one of the first times I’ve seen a card’s good standing status tied to some external monthly subscription, and I’m not totally sure how this will work. If you decide not to pause your Robinhood Gold subscription for a month or two, do they close your credit card? Who knows.

Fortunately, Robinhood Gold is only $5/month, and if you already invest with Robinhood, it’s a bit of a no brainer: you’ll get a free $1k in margin, lower margin interest rates, 5% on uninvested cash, and more.

This card earns cash back, not points

In the world of cash back cards, Robinhood’s 3% universal cash back might as well make it the new king. But cash back cards are the little league since they aren’t nearly as flexible or value as cards earning points. That’s because the value of cash back is fixed but the value of points is variable. 1¢ of cash back is 1¢ of cash back and will always be just 1¢ of cash back. But depending on your skill and luck, 1 point could be redeemed for anything from 1¢ to 10¢. That means a card that earns a standard 1x points on everything could be the equivalent of earning 1% to 10% cash back depending on how you use those points.

Shreycation is all about helping you learn how to use your points well. With some basic knowledge, it’s pretty easy to achieve a rate of at least 2¢/point on virtually all of your award travel redemptions. That means a card like the Chase Freedom Unlimited that earns 1.5x points on everything nets me at least 3¢ per dollar I spend. On the other hand, the Robinhood Gold card also earns me 3¢ per dollar, but that’s a hard cap — it’ll only earn me 3¢ per dollar.

No sign up bonus or intro 0% APR

The Robinhood Gold account comes with no sign up bonuses or introductory 0% APR rates whatsoever. For other cards in this category, there’s usually a ~$200 sign up bonus, and at least 1 year of 0% APR.

If you intend on actively using this card for many years, the lack of a bonus might not be a huge issue today, but do note that it’ll take almost $7k in spending to match the free sign up bonus of its peers.

The bigger issue is the lack of a 0% APR intro period. Right now, if you rack up a $10k balance on a card with 12 months of 0% APR, you can instead invest all that money in a high yield savings account and earn 5% over the course of the year. That’s basically the equivalent of a 5% cash back on everything. You’re forgoing that option if you choose to spend more on a Robinhood Gold card.

A word of caution

The card has some pretty awesome perks and a killer cash back earning structure today, but these aren’t necessarily guaranteed in the future, especially for younger companies like Robinhood.

We’ve seen this in the past with cards like the Uber Visa Card, which used to give 4% on dining, 3% on travel, and 2% on Ubers — pretty awesome for a no annual fee card. But over time, the card kept getting nerfed and eventually became less and less compelling until it was finally shuttered.

That’s not to say this will necessarily happen to the Robinhood card, but it’s good to know that this may not last in perpetuity.

If you’re enjoying our breakdown of the Robinhood Gold card, subscribe for more! I’ll be writing about my favorite underrated cards and hacks to save you money.

Who should actually get this card?

Beginners and people who don’t wanna deal with points.

By itself, this card ticks a lot of boxes: great cash back on everything, solid protections, no transaction fees. This makes it an excellent card for beginners.

I’ve waxed poetic about the value of points above, but if care more about simplicity, a card that gives 3% cash back without having to think about it is a pretty solid middle ground. And if you don’t travel much in the first place, you won’t be able to extract much of the value of your points anyway — cash back could be the better option.

The Robinhood Gold card also effectively renders many other cash back cards obsolete, meaning you can double down on simplicity and get by with fewer cards. Most cash back fans can now get by with just two cards: (1) the Robinhood Gold, and (2) some card that earns 5% on seasonal categories (e.g. Chase Freedom Flex, Discover It).

People who don’t have a great catch all card yet

A key element of any good personal card portfolio is a “catch all” card that earns > 1% cash back or 1x points on non-category spend. In other words, it’s cool if you have swanky cards that earn 3% on travel and dining (“category spend”), but if you also drop $3000 a year on Rumble Boxing or have a crippling shopping addiction, it would be nice to earn boosted cash back here too.

Catch all cards usually don’t have highly boosted cash back on special categories, but they do have slightly boosted cash back on everything. Up till now, 2% was about the best you could do for a catch all cash back card (RIP Citi Double Cash), but now Robinhood has blown this out of the water with its 3% and is the obvious choice.

There’s one big caveat: if you have one of the premium travel cards — a Chase Sapphire, Amex Gold or Platinum, or a Capital One Venture — it might make sense to choose a card in those ecosystems as your catch all card. That’s a topic for another Shreycation issue, but generally you’ll get more value (and better purchase protections) on those cards than the Robinhood Gold.

People who hate taxes but like math

Death and taxes may be the only two things guaranteed in life, but the Robinhood card can help you reduce your annual subscription to Uncle Sam.

The IRS lets you pay your outstanding taxes using a credit card. They’ll charge you 1.8% for this privilege, but if you’re using a card that gives you 3% cash back…you see where I’m going here.

Courtesy of Robinhood, you can now enjoy a 1.2% discount on income taxes you pay directly. If most of your income comes from W-2 earnings, your employer is already withholding most of your income taxes for you and you’re likely not paying much on tax day, meaning this hack probably won’t be as useful. But if you have lots of 1099 earnings (e.g. from freelancing or side gigs), have high capital gains, or own a business and pay quarterly taxes, you’re usually paying a large chunk of your tax liability directly. By using the Robinhood Gold card to pay, you could keep hundreds of extra dollars in your pocket.

We can go one step further for a really cheeky version of this hack. Since you’re paying taxes with a credit card, you have at least a whole month to pay down the balance while avoiding an interest charge. So maybe instead of paying down the card immediately, stick that tax money in a 5% APY high yield savings account for a month, and then pay your card. 5% APY earned for one month translates to a ~0.4% ROI, boosting your effective tax discount to 1.6%.

You can also do this hack with the Paypal Mastercard (which gives you 3% cash back on Paypal transactions), but the Robinhood Gold card is a way more versatile card to have in your wallet.

If you’ve decided the Robinhood Gold is the way to go for you, you can use the link below to add yourself to the waitlist. We’ve also got some alternative cards below that are worth your consideration!

Other cards that might be worth instead

Chase Freedom Unlimited

I’ve mentioned this card a few times in this article, but the Chase Freedom Unlimited is a very compelling alternative to the Robinhood Gold if you’ve already got a Chase Sapphire Preferred or Reserve.

1.5% cash back on everything…BUT if you have a Chase Sapphire card, you can opt to receive 1.5x points instead. And as we discussed above, 1.5 pts is easily worth at least 3¢.

Also, 5x on travel booked through Chase Travel, 3x on dining, 3x on drugstores

Many of the same protections as the Robinhood card, minus return protection.

Sign up bonus of 20000 points and 15 months of 0% APR.

No annual fee.

Wells Fargo Autograph

Wells Fargo has really been stepping up its game lately and has started building their own points ecosystem with their own transfer partners. I’ll write more about it later, but their starter card is the Wells Fargo Autograph and its quite compelling.

3x points on many categories: dining, gas, travel, transit, streaming, and phone services. For some of you, this might be the majority of your spend (groceries and shopping are notably missing though).

Sign up bonus of 20000 points and 12 months of 0% APR.

Doesn’t have as many protections as the Robinhood Gold, but does offer cell phone protection.

No annual fee.

Thanks for reading! At the end of the day, Robinhood is selling simplicity, but credit cards don’t exist in a vacuum — they exist in your wallet with your other cards. I hope this article helped breakdown the Robinhood Gold card, and gives you a good sense of whether its right for you. As always, feel free to add questions in the comments, and share with a friend.

Bon Voyage,

Shrey